In Q1 2026, the largest European fuel networks are not arguing about whether the forecourt has to change. They are arguing about which layer to build first. The dominant industry conversation, led by hardware vendors and consultancies, frames the smart forecourt around pumps, EV chargers, and food-to-go. That framing is incomplete.

A smart forecourt is one where every fuel stop becomes an identifiable, reachable customer, with that identity feeding loyalty, fleet invoicing, retail media, and post-visit engagement across every brand and every site. The relationship layer is what determines whether the rest of the capex actually returns.

According to McKinsey, the global forecourt value pool is projected to grow from roughly $22B in 2019 to $30B by 2030, with almost all the upside in non-fuel revenue that depends on knowing who the customer is.

What Is A Smart Forecourt?

A smart forecourt is a fuel station where every customer transaction, at the pump, in the shop, at the EV charger, or via a fleet card, is tied to an identifiable customer profile, and where that identity feeds loyalty, retail media, fleet invoicing, and post-visit engagement.

It is distinct from a “connected” forecourt, which describes hardware and IoT integration, and from a “digital” forecourt, which usually refers to payments and self-service. Connectivity and digital payments are inputs. The smart forecourt is what they are inputs to.

Why The Forecourt Is The Most Anonymous Retail Format

The forecourt is the most anonymous retail format in modern retail, and the cost of that anonymity is rising in 2026. Customers transact in under five minutes, often without entering the shop. There is no app default, no checkout queue, no loyalty card prompted at the till. According to industry estimates cited by Pixel Inspiration, up to 70% of fuel customers drive away without setting foot inside the shop, leaving the highest-margin part of the site untouched.

The anonymity now hides a more expensive segment than it used to.

High-income households increased convenience-store spend by 52% year on year, while households earning under $75,000 reduced spend by 11%. The high-spending visitors are exactly the ones operators cannot see at the pump. High-income drivers fuel faster, enter the shop less often, and skew toward fleet cards and pay-at-pump options that bypass any in-store identification moment. Loyalty has not closed the gap.

The same NACS-cited consumer research finds that even mature programs sit at roughly a 50% active-engagement ceiling, with only about half of enrolled members using their loyalty programs consistently. Customer behaviour is more volatile too: the average driver now visits 2.6 different fuel stations a month, up 7% year on year. Operators are investing record capex in food, EV, and retail media while still running an anonymous front end.

The Four Layers Of A Smart Forecourt

The smart forecourt is built in four layers, in this order:

- Identity at the checkout. Every visit becomes an identified customer.

- Engagement after the visit. That identity becomes a channel.

- Fleet, served properly. Compliant cross-border invoicing happens at the dispenser, not at month-end.

- Retail media that actually targets. Attention is sold against known customers, not broadcast to anonymous ones.

The order matters. Identity is the substrate, engagement is the consequence, fleet is the parallel B2B track, and retail media is where the prior three compound into revenue.

Identity At The Checkout

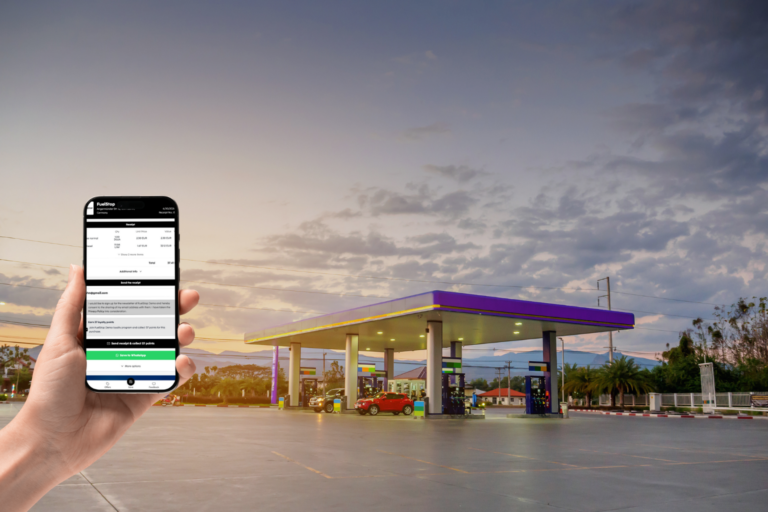

Identity at the forecourt happens through the receipt, not through an app. The receipt is the only universal touchpoint at a fuel station: every customer gets one, every transaction generates one, and no download is required to receive it. Moved digital, it becomes the identification layer the operator never had.

How do digital receipts work at fuel stations?

The mechanic is straightforward. At the till, the customer scans a QR code or taps an NFC marker. A receipt loads in their browser, in their device language. They can save it, forward it, or opt in to hear from the operator. No app install. No friction at a moment when the customer wants to leave.

Across refive’s deployments, 60-70% of customers opt for the digital receipt, and roughly half of them opt in to be reached again.

What identification unlocks is the rest of the framework: closed-loop attribution between pump and shop, visibility into the high-spending segment NACS data flags as the growth driver, and a way to onboard customers into a loyalty program at their own pace. The regulatory tailwind is real. Germany’s Belegausgabepflicht is moving toward mandatory digital receipts by 2029. France banned automatic paper printing under the AGEC law in August 2023. Italy approved a phased ban in June 2025, with large retailers transitioning by January 2027 and all merchants by 2029. The receipt is going digital regardless.

The question is whether operators use the transition to identify customers or just to print less paper.

Also Read: What Is Progressive Profiling in Retail? A Guide for CRM, CX & Marketing Teams

Engagement After The Visit

Engagement after the visit is the layer where forecourt loyalty stops being theoretical. Once the customer is identified, the receipt becomes a channel: a place to onboard them into, potentially, Shell GO+, BPme, Circle K Inner Circle, or ExxonMobil Rewards+; a place to prompt a Google review when satisfaction is high and route feedback inward when it is not; a place to deliver a localised offer tied to the station they actually visit.

The post-visit window is where loyalty either compounds or dies.

Industry research identifies the 90 days after enrollment as the window that decides whether a member becomes active or dormant, and operators who use that window for low-friction, contextual prompts have reported active-engagement rates well above the category benchmark. Mature programs already exist but they all face the same enrollment-vs-engagement gap.

The structural gap is sharper in mid-market and independent retail. There is no definitive leader in forecourt loyalty for operators below the major-network scale, and most EPOS providers do not ship loyalty as a native capability. For independent groups running 8 to 100 sites, often across fuel, convenience, and food-service formats, the practical question is not which loyalty platform but how to identify the customer once and use that identity across all three formats. Identification at the receipt is the route into that conversation.

The global loyalty market is projected to keep growing from roughly $13B in 2024 to $41B by 2032, with the fuel and convenience share weighted toward operators who solve the activation step.

Fleet, Served Properly

Fleet is not a phase-two problem at the forecourt. It is a primary revenue stream. Commercial vehicles account for a meaningful share of European fuel volume, and the operational cost of serving them well sits squarely on the receipt and the invoice.

A smart forecourt handles fleet at the moment of payment, not at month-end.

How does e-Rechnung work at fuel stations?

e-Rechnung is the German term for the structured digital invoice now mandated across most major European markets. At the point of sale, it means that when a fleet driver pays with a fleet card, the transaction triggers a compliant e-invoice in the right national format, routed directly to the fleet’s ERP. No paper. No end-of-month chase.

The 2026-to-2028 mandate environment makes this layer urgent. In Germany, all businesses have been required to receive e-invoices since January 2025, with mandatory sending for firms above €800k turnover landing 1 January 2027 in the XRechnung and ZUGFeRD formats covered by EN 16931.

France launches its mandate on 1 September 2026 for large and mid-sized firms using Factur-X. Italy has run B2B e-invoicing through FatturaPA via the SDI system since January 2019. Poland makes KSeF mandatory for large taxpayers on 1 February 2026. Belgium’s Peppol-based mandate landed 1 January 2026.

For a fuel network with cross-border traffic, German fleet drivers running into Czech, Polish, Austrian, and Hungarian markets, format complexity is the operational pain. The smart forecourt absorbs that complexity at the moment of payment.

Retail Media That Actually Targets

Retail media at the forecourt is the layer where the prior three compound. The captive moment is real: 5 minutes at an ICE pump, 15 to 20 minutes at a 350kW high-power charger, longer at slower public chargers. Operators have noticed.

What is retail media at the forecourt?

Retail media at the forecourt is the sale of advertising inventory, on pump-side screens, in-store digital signage, and increasingly on the digital receipt itself, against the dwell time of fuel and convenience customers. The category is growing fast: in-store retail media expanded roughly 47% in 2025, and the global retail media category is projected to cross $100B by 2027.

The retail-media-at-the-pump conversation in 2026 has focused on screens. Most of the inventory those screens carry is broadcast at an audience nobody can identify. That is fine for awareness. It is structurally weak for closed-loop attribution, which advertisers are starting to demand. The receipt is a different kind of inventory: targeted at an identified customer, delivered post-purchase, contextual to what they actually bought.

What Changes When EV Charging Arrives

What changes when EV charging arrives is dwell time, and dwell time changes the customer-relationship math. ICE fueling runs under five minutes. A 350kW high-power charger session runs 15 to 20 minutes. Slower public charging runs 30 minutes to several hours. Longer dwell does not threaten the framework. It makes every layer more valuable.

How is EV charging changing fuel retail?

The new KPI is profit per kWh, not just margin per litre, and it is calculated to include attached revenue from coffee, food, retail media, and loyalty. The EU’s Alternative Fuels Infrastructure Regulation (AFIR) requires fast-charging pools every 60 kilometres along TEN-T routes by 2030, forcing capex regardless of operator strategy.

Operators who treat the EV transition as a customer-relationship investment, not a hardware investment, will compound the longer dwell time into identification, repeat visits, and attached revenue.

What ORLEN Deutschland’s Rollout Shows

ORLEN Deutschland now operates more than 600 stations across four brands (ORLEN, STAR, Famila, and Star Express) and rolled out the customer-identification layer in under five weeks, with no new hardware. The deployment is one of the largest of its kind in European fuel retail and shows what the four layers look like in practice across a multi-brand network.

Identity sits at every station: customers receive a digital receipt at the terminal via QR scan, in their device language, no app required. Engagement runs through the same channel: customers can opt in to hear from ORLEN directly. Fleet is handled at checkout, with cross-border drivers receiving fully compliant digital invoices that meet the tax requirements of every market they fuel in. Retail media inventory is now targetable against identified customers, not just broadcast.

The integration ran via ORLEN’s existing HUTH POS and the tankstar SDK, powered by refive’s platform, with no infrastructure changes. At full run, the rollout is expected to remove around 36,000 kilometres of thermal paper, 300 tonnes of CO2, and 132 tonnes of waste annually.

A smart forecourt is a fuel station where every customer transaction, at the pump, in the shop, at the EV charger, or via a fleet card, is tied to an identifiable customer profile. That identity feeds loyalty, retail media, fleet invoicing, and post-visit engagement. It is the customer-relationship layer that connects the hardware investments operators are already making.

A connected forecourt describes hardware and IoT integration: networked pumps, real-time wetstock monitoring, payment terminals, EV chargers tied to a back office. A smart forecourt is built on top of that connectivity and adds the customer-identification layer. Connected is about uptime and data flow between machines. Smart is about identifying, engaging, and serving the customer behind every transaction.

At the till, the customer scans a QR code or taps an NFC marker. A receipt loads in their browser, in their device language, no app required. They can save it, forward it, or opt in to hear from the operator. The receipt is delivered in seconds and complies with the German Belegausgabepflicht, French AGEC law, and Italy’s phased digital-receipt regulation.

When a fleet driver pays at the till with a fleet card, the transaction triggers a compliant e-invoice in the right national format (XRechnung or ZUGFeRD in Germany, Factur-X in France, FatturaPA in Italy, KSeF in Poland, Peppol in Belgium), routed directly to the fleet’s ERP before the driver pulls away. No paper, no manual reentry.

Retail media at the forecourt is the sale of advertising inventory across pump-side screens, in-store signage, and the digital receipt, against the dwell time of fuel and convenience customers. The most valuable inventory targets identified customers and delivers closed-loop attribution.

EV charging extends customer dwell time from under five minutes at an ICE pump to 15 to 20 minutes at a 350kW high-power charger, and longer at slower units. Operators are redesigning sites around longer stays: better food, better seating, retail media that earns attention. The KPI shifts to profit per kWh, including attached revenue from food, retail, and loyalty.

ORLEN Deutschland, for example, is now live with digital receipts across more than 600 stations and four brands. Other European networks have piloted or expanded digital-receipt programs alongside their loyalty apps, including operators using Shell GO+, BPme, and OMV’s mobile platforms. Multi-brand operators in DACH and CEE markets are the most active segment in 2026.

refive is the customer-engagement platform behind the receipt at ORLEN Deutschland and a growing set of European retailers. The conversations that tend to land are with operators scoping the customer-identification layer for the next 24 months of forecourt investment, multi-brand networks planning a single experience across sites, and teams asking what the receipt could carry beyond compliance. If that is the conversation you are in, we would be glad to talk.