A business driver fills the tank and asks for an invoice at the counter. What comes back is a faded thermal receipt, a queue while a cashier retypes the details by hand, or a promise that the invoice will follow at month-end. Fleet e-invoicing exists to end exactly that: a compliant invoice issued at the pump, in the moment of payment, rather than negotiated at the till.

For finance and fleet leaders, that counter moment is a small recurring tax on every business fill-up. Multiply it across a fleet, a year, and a network of sites, and the cost shows up as VAT that never gets reclaimed, invoices that arrive late or wrong, and drivers who lose ten minutes they did not have.

This piece sets out what a compliant invoice actually requires, the four places the counter process breaks, the German and EU deadlines that turn the problem from a nuisance into a liability, and how issuing a compliant e-invoice at the point of payment fixes it for every business customer, not only the ones carrying a fuel card.

What is fleet e-invoicing?

Fleet e-invoicing is the issuance of a compliant, structured electronic invoice to a business driver or fleet for a fuel or charging purchase, so the cost and its input VAT can be reclaimed. In Germany that means an invoice built to the European EN 16931 standard, in a format such as XRechnung or the hybrid ZUGFeRD. A PDF and a printed till receipt are not the same thing.

The word that matters is structured. A structured e-invoice is a machine-readable file, usually XML, that carries every mandatory VAT field in a defined place, so a buyer’s accounts payable system can read and post it without anyone retyping it. According to the European Commission’s e-invoicing guidance for Germany, the accepted formats are XRechnung (pure XML), ZUGFeRD (a PDF with embedded XML), and Peppol BIS, all built on EN 16931.

A fuel receipt is a printed record of a sale. A compliant invoice is a structured tax document. The gap between the two is where input VAT recovery succeeds or fails, and it is exactly the gap the counter has always handled badly.

Why a fuel receipt won’t get the VAT back

A fuel till receipt cannot recover input VAT because it is not a structured invoice carrying the VAT fields a tax authority and a buyer’s accounts payable system require. It is a B2C document. For a business to deduct the VAT, it needs a proper invoice in the buyer’s name with the mandatory tax detail.

This is not a future problem. German tax guidance tracking the new rules is consistent: once the relevant deadline passes, a paper or unstructured invoice will not support an input VAT deduction, and a buyer can be left chasing a corrected document before it can reclaim anything (Marosa, 2026). The German VAT Act also allows administrative fines of up to €5,000 per offence for invoice and retention breaches, though for most finance teams the larger cost is the blocked or delayed deduction, not the penalty.

The practical failure looks mundane. A driver hands accounts a thermal slip that has half-faded in a glovebox. The till receipt has the station’s VAT number but not the buyer’s. The cashier issued a hand-typed invoice with a transposed figure. Each one is a small reclaim that stalls, and at fleet scale the small reclaims add up to real working capital sitting unclaimed.

How big is B2B at the forecourt?

Business fuel is a large, structural share of forecourt volume, not a fringe. Fleets, company-car drivers, cross-border hauliers, and the long tail of tradespeople and SMEs filling up on business all need a compliant invoice, and they buy fuel constantly.

The scale is in the vehicle base. The European Automobile Manufacturers’ Association’s 2026 Vehicles on European Roads report counts roughly 38 million commercial vehicles, vans, trucks and buses, on EU roads. Fuel also carries one of the highest business-to-business shares of any retail category, which is why invoicing failure is more expensive here than in most stores.

Some of this volume already runs on fuel cards from DKV Mobility, UTA Edenred, Shell, and others, which consolidate purchases into a single tax-recognised invoice. That covers cardholders on-network. It does not cover the company-car driver paying by corporate card, the SME owner filling a van, the visiting driver off their usual network, or anyone fuelling across a border. For an operator focused on serving fleets properly on the forecourt, those drivers are the ones still stuck at the counter.

Where the counter invoice breaks: four failure points

The counter invoice fails in four predictable places, and each one delays or blocks the driver’s VAT recovery. Naming them makes the fix obvious.

1. The thermal receipt that is not an invoice. A standard till receipt is a B2C record, not a structured invoice, and it fades. German VAT law does exempt small-value invoices under €250 from the structured-format requirement, so a single car fill-up can use a simplified document. But truck diesel fills and most fleet transactions run well above €250, where a proper invoice is required and a thermal slip will not do.

2. The counter queue. When the receipt is not enough, the driver waits while a cashier opens a separate invoicing screen and retypes the company name, address, and VAT number by hand. It is slow, it is staffed only when the shop is staffed, and manual entry is where most invoice errors begin.

3. Month-end batching. Many networks defer the problem by collecting transactions and issuing invoices in a month-end run. That delays every reclaim by weeks and batches the errors together, so one wrong VAT number can hold up a whole statement.

4. Cross-border format mismatch. A driver fuelling in Germany, France, Italy, and Poland in the same week meets a different invoice regime in each: XRechnung or ZUGFeRD in Germany, Factur-X in France, FatturaPA in Italy, KSeF in Poland, with Peppol as the common transport layer. A counter process built for one country cannot produce the right document in the next.

The compliance clock: Germany 2027 to 2028, ViDA 2030

Germany already requires every business to be able to receive structured e-invoices, and phases in mandatory issuing from 2027; the EU’s VAT in the Digital Age reform then makes a valid e-invoice a condition for reclaiming the VAT on intra-EU business transactions. The deadlines turn a long-standing annoyance into a dated liability.

Under the Growth Opportunities Act, the German Federal Ministry of Finance set a clear sequence: businesses have had to be able to receive EN 16931 e-invoices since 1 January 2025; issuing becomes mandatory for firms above €800,000 in prior-year turnover from 1 January 2027, and for all firms from 1 January 2028. France banned automatic receipt printing in 2023 and Italy’s phased digital mandate runs from 2027, so a cross-border network feels the change on several fronts at once.

The bigger shift is at EU level. Under the VAT in the Digital Age reform, adopted as Council Directive (EU) 2025/516 in March 2025, structured e-invoicing for intra-EU business transactions becomes mandatory from 1 July 2030, and holding a valid e-invoice becomes a condition for deducting or reclaiming the VAT on them. At that point the compliant invoice stops being good practice and becomes the thing that lets the money be recovered.

The fix: a compliant e-invoice at the point of payment

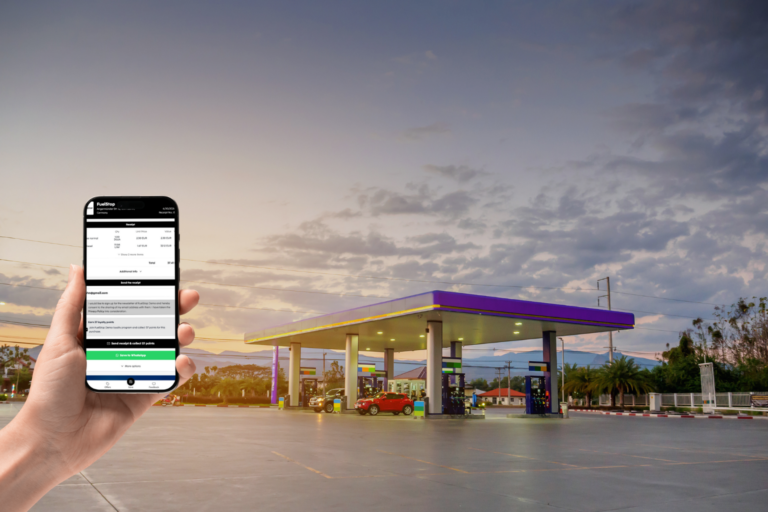

A compliant e-invoice issued at the point of payment closes all four failure points, because the document is created where the transaction and the buyer’s details already meet. The driver enters their company details once, at the pump or the till screen, and self-serves a structured invoice in the right format.

It works through the receipt workflow rather than a separate counter process. The driver scans a QR code, taps an NFC point, or uses the on-screen flow, all browser-based with no app to download, and the compliant invoice is generated and sent. Because it rides POS-agnostic digital receipt software, it works across mixed estates and mixed vendors, and it serves every business customer, not only fuel-card holders.

Map it back to the four failures. The faded thermal slip is replaced by a structured invoice (point 1). The counter queue disappears because the driver self-serves (point 2). Issuance happens in real time, not at month-end, so reclaims start immediately (point 3). And the format is selected for the country of purchase, so a cross-border driver gets XRechnung, Factur-X, or FatturaPA as needed (point 4). A receipt archive lets staff find and reissue a past invoice from partial detail, so the rare exception still resolves without a paper chase.

This is the capability refive ships as part of the receipt workflow, alongside the receipt archive and a customer-facing receipt finder, and it is in production today.

Proof: met as an Orlen RFP requirement

When Orlen put its receipt and invoicing requirements out to tender, a compliant e-invoice issued through the receipt workflow was a stated requirement, not an optional extra. The network needed to serve its business and fleet customers properly, and counter invoicing did not meet the bar.

refive met that requirement and deployed it as part of the receipt rollout across Orlen’s network of more than 600 stations, displacing an incumbent on the strength of the response. The deployment is recent and still building, so this is a story about scale and about winning a demanding RFP, not a claim about outcome numbers we do not yet have. The point for a finance or fleet leader is narrower and more useful: a major network treated point-of-payment e-invoicing as a procurement requirement, because the counter could not deliver it.

A counter built for cash, in a structured-invoice world

The forecourt counter was designed for cash and paper, in an era when a printed slip was enough. The rules have moved: from 2027 in Germany and 2030 across the EU, the compliant invoice is what lets a business reclaim its fuel cost and VAT, and that document now has to originate at the moment of payment, not be negotiated at the till. The operators who move issuance to the pump fix the problem for every business customer at once.

To see what point-of-payment e-invoicing would look like across your network, book a fleet-invoicing review.

Frequently asked questions

Fleet e-invoicing is issuing a compliant, structured electronic invoice to a business driver or fleet for a fuel or charging purchase, so the cost and input VAT can be reclaimed. In Germany it means an EN 16931 invoice in a format such as XRechnung or ZUGFeRD, issued digitally rather than typed up at the counter.

A till receipt is a B2C record, not a structured tax invoice in the buyer’s name with the mandatory VAT fields. For business purchases above €250, German VAT rules require a proper invoice, and once the e-invoicing deadlines pass an unstructured document will not support an input VAT deduction.

Both are valid. XRechnung is a pure XML file built for automated processing; ZUGFeRD is a hybrid that pairs a readable PDF with embedded XML. Both meet the European EN 16931 standard, and Peppol is a common way to transmit them. The buyer’s system usually decides which format is preferred.

Fuel cards from DKV Mobility, UTA Edenred, and others consolidate cardholder purchases into a tax-recognised invoice, which works well for on-network fleet customers. It does not cover company-car drivers paying by corporate card, SMEs, off-network stops, or ad-hoc business fill-ups, who still need an invoice from the station.

Under the Growth Opportunities Act, businesses have had to receive structured e-invoices since 1 January 2025. Issuing becomes mandatory for firms above €800,000 turnover from 1 January 2027, and for all businesses from 1 January 2028. B2C till receipts sit outside this mandate.

The EU’s VAT in the Digital Age reform, adopted in March 2025, makes structured e-invoicing mandatory for intra-EU business transactions from 1 July 2030 and makes a valid e-invoice a condition for deducting or reclaiming the VAT on them. For cross-border fleets, the compliant invoice becomes the document that lets the VAT be recovered.

A driver fuelling across Germany, France, Italy, and Poland meets a different format in each market: XRechnung or ZUGFeRD, Factur-X, FatturaPA, and KSeF, with Peppol as the shared transport layer. Issuing the invoice at the point of payment lets the correct national format be selected per transaction.

Yes. A point-of-payment workflow can deliver the invoice through a browser, opened by a QR code, an NFC tap, or an on-screen prompt, with no app to download. Because it is POS-agnostic, it can run across a mixed network without replacing existing forecourt systems.