A single customer view is one unified profile per customer: identity, purchases, and engagement from every channel, held in a single record your CRM or CDP can act on. Most variety and lifestyle retailers believe they have one. What they actually have is a single-channel view.

Look at the two halves of your own database. Your online customer is fully documented. You know her email address, her order history, the products she browsed on Tuesday, and which campaign brought her in. Your in-store customer bought more this year, visited more often, and your systems have no idea she exists.

The imbalance would matter less if the store were a side channel. It is the opposite. For variety and lifestyle retail, physical stores carry the large majority of revenue, and the shoppers walking through them are exactly the people your CRM was built to reach. According to EY research published by Shopify in 2025, known customers spend up to three times as much per order as anonymous shoppers. Your store is full of customers who could be known and are not.

This post covers why the gap exists, what it costs in three specific places, and how to close it with the infrastructure you already own.

Why does omnichannel retail still leave the in-store customer anonymous?

Because online channels generate first-party data as a by-product of how they work, and stores never have. Omnichannel retail unified stock, fulfilment, and brand experience across channels. Identification never made the same journey. It stayed where it was born: in the browser.

Every e-commerce session starts with a mechanism that can identify someone. An account login, a checkout email, a cookie, an attribution pixel. Nobody at your company had to do anything for that data to arrive; the channel produces it by default. A store transaction produces a basket, a payment, and a receipt. None of the three carries an identity unless someone adds one deliberately.

This is not an e-commerce maturity problem. The variety and lifestyle segment went digital early and seriously; Søstrene Grene launched its first webshop in March 2020 and has since opened webshops across more than a dozen markets. The digital channel is identified end to end. It simply carries the smaller share of transactions, which means the identified slice of the customer base is a minority by construction.

The usual answer to the in-store side has been loyalty. It works, up to a point, and the point is enrolment. A loyalty programme identifies members, and members are always a minority of transactions. Signing up takes effort, the value exchange has to be renewed constantly, and even a well-run scheme leaves the majority of till transactions unattributed. Everyone else pays and leaves as a stranger.

What makes this worth stating plainly is that the retailers living with the gap are sophisticated operators, running exactly the stack the martech industry recommends. Søstrene Grene selected mParticle as its customer data platform in 2022 to unify data across online and in-store touchpoints, and runs its campaigns through Salesforce Marketing Cloud. HEMA launched its More HEMA programme in 2017 and grew it into the second-largest loyalty scheme in the Netherlands, with customer data centralised through Selligent and Salesforce, according to the Springbok Agency case study. Flying Tiger Copenhagen and Normal operate in the same brand-led, digitally mature segment.

These companies did the CDP work. The gap persists anyway, because a CDP unifies the data it receives, and the store sends almost nothing. The large majority of in-store customers still complete their purchase and walk out without any identifier attaching to the transaction. The stack is fine. The input is missing.

What does the in-store data gap cost a variety retailer?

The cost shows up in three places: you cannot personalise for people you cannot recognise, you cannot attribute marketing to sales you cannot connect, and you cannot value customers you only half see. Call them the three blind spots of an incomplete single customer view: personalisation, attribution, and lifetime value.

Why can’t you personalise for in-store customers?

Personalisation needs history, and anonymous transactions create none. A shopper can visit weekly for a year, and to your marketing systems her eleventh visit looks identical to her first: no preferences, no basket record, no channel to reach her before the twelfth.

Consider what the missing history would power. A shopper who buys craft supplies and children’s items on every visit is a perfect audience for a new-arrivals notification in exactly those categories, the kind of campaign this segment’s marketing teams already run beautifully for online customers. Without an in-store identity, she is not in any segment. The campaign exists; she is simply not addressable by it.

The commercial weight of that blindness is documented. The same EY research reports that known customers drive up to 61 percent of repeat purchases. Repeat business concentrates among the customers a retailer can recognise and reach. In-store, that group is a fraction of the people actually repeating, which means the majority of your most loyal shoppers receive precisely none of the personalisation budget built for them.

Why can’t you attribute online marketing to store sales?

Because the conversion happens in a channel that reports nothing back. Digital campaigns drive store visits every day, and when the resulting purchase is anonymous, the loop never closes. The campaign gets judged on online conversions alone, which systematically undervalues the ads doing the hardest work.

Drive-to-store formats make the problem concrete. Local campaigns for a new store opening, a seasonal drop, or a weekend footfall push get measured today through proxies: impressions, map clicks, footfall estimates. Whether the person who saw the ad actually bought, and what she bought, stays unknown, so the formats that most directly serve a store-led business are the ones evaluated with the least evidence.

The stakes rise with acquisition costs. Average customer acquisition cost reached $226.38 in 2024, up 7 percent year on year, according to figures cited in Shopify’s 2025 retail analysis. Paying more per acquired customer while remaining blind to the largest conversion channel is an expensive way to run marketing. Online-to-offline attribution is not an analytics luxury; it is how the biggest line in the budget gets measured honestly.

Why is customer lifetime value wrong without store data?

Because the model only counts the channel it can see. A customer who buys online twice a year and in-store twice a month is recorded as a low-value occasional shopper. Every decision built on that number inherits the error: segmentation, reactivation triggers, campaign spend caps, even the business case for retention itself.

The distortion is largest exactly where variety retail is strongest: frequency. Søstrene Grene refreshes its assortment with hundreds of new items arriving on Thursdays, a rhythm designed to bring shoppers back week after week. Treasure-hunt merchandising generates the visit patterns that make lifetime value compound, and those visits are the ones the LTV model cannot see. EY’s research puts the scale of what is being mismeasured in context: known customers account for 76 percent of in-store sales growth.

The mirror image of mismeasured value is invisible churn. When a weekly store visitor stops coming, no system registers it, no reactivation flow triggers, and the revenue quietly disappears from a customer the database never contained. Online, that same lapse would fire a win-back email within the month. In-store, the retailer’s most valuable defections are the ones it cannot detect.

How do you identify in-store customers without an app or a loyalty card?

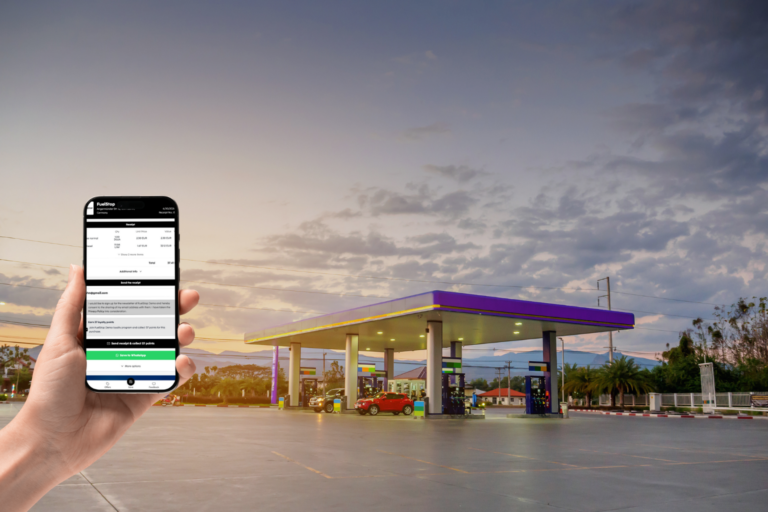

At the receipt. Every transaction already produces one, which makes it the single touchpoint with universal coverage: no download, no enrolment, no change to how anyone pays. Replace the printed slip with a QR code at the point of sale, and the receipt becomes the moment omnichannel customer data starts flowing from the till.

The mechanics are short. The customer scans the code and the receipt opens in the browser. That scan creates an anonymous profile linked to the full basket. On the receipt page, the customer can leave an email address and a marketing opt-in, which upgrades the anonymous profile to a known one. Identification happens as a side effect of a service the customer wanted anyway.

The architectural point matters more than the mechanics, and it is the reason this belongs in a CRM lead’s roadmap rather than an IT replatforming plan. Receipt-led identification does not replace anything you run. It is an input layer. The profiles and purchase data flow by API into the CDP and campaign tools already in place, whether that is Salesforce Marketing Cloud, mParticle, Selligent, or a warehouse-native setup. Your CDP stays the system of record; it finally receives the in-store half of the data it was bought to unify. This is the model refive runs in production for physical retailers, feeding in-store identification into existing stacks rather than alongside them.

Two practical objections come up whenever this segment evaluates receipt-led capture, and both have short answers. The first is checkout speed. High-footfall formats live and die by queue pace, and any capture method that adds a dialogue at the till fails on contact. The receipt model adds no step: the QR code appears where the paper receipt used to, the scan happens after payment on the customer’s own time, and the cashier does nothing new. The second is rollout effort. Because capture rides on the receipt rather than new hardware, deployment is POS-integration work measured in weeks, and it scales across an estate the way receipt formatting does, uniformly.

Consent is handled at the same moment. The opt-in is explicit, tied to a real interaction, and recorded per customer, which is a cleaner GDPR position than most legacy capture methods can claim. For teams already operating under GDPR with a CDP, the consent flow slots into the preference management they run today.

The prize is the one this segment’s own leaders keep naming. When Søstrene Grene announced its CDP selection, Rasmus Skjøtt, the company’s Chief Digital Officer for omnichannel, put it directly: “Gaining a unified view of each customer will help us provide shoppers with the most relevant information and product deals whether they are shopping online or in-store.” The unified view is the agreed destination. The receipt supplies the half of the map that has been missing.

What changes when the profile is complete?

A complete profile turns the omnichannel customer experience from a slogan into an operating reality, because every downstream system finally works from whole information. Each blind spot reverses.

Personalisation extends to the store majority. The weekly shopper from the personalisation section now has a profile, a history, and a reachable channel, so campaigns, recommendations, and offers can reflect what she actually buys rather than what she happens to buy online. The receipt that identified her can carry the next offer as well; we cover that mechanic in how digital receipts become marketing tools.

Attribution closes the loop. In-store purchases connect back to the campaigns that drove them, so channel budgets get set against real performance instead of the online-only slice of it.

Lifetime value becomes honest. The models finally include store frequency, which re-ranks who your best customers are, and reactivation programmes gain an audience that previously did not exist in the database: the store-only customer who lapsed silently.

Segmentation improves as a by-product. Segments built on complete purchase behaviour, both channels, full frequency, describe real customers instead of their online shadows, and campaign performance measurement inherits the same correction: results get read against everything a customer did, including the store visit the campaign actually caused.

There is a compounding effect worth naming. Each identified transaction enriches the profile, which improves the next campaign, which drives the next identified visit. Online retail has run on that flywheel for two decades. Completing the single customer view lets the store join it.

What does this look like in practice?

Extra Shop, a Belgian home and décor retailer with around 55 stores, runs receipt-led identification in production. Digital receipts are live across the estate, and the identification layer feeds customer engagement from the store side, the segment’s most common gap. The deployment is the variety and lifestyle pattern in miniature: a brand-led retailer with real digital ambition, adding the in-store input its customer data setup lacked.

On capture performance, refive’s deployment data across retailers shows 40 to 70 percent or more of customers taking the digital receipt via QR scan, with 50 to 60 percent of those scanners providing an email address and marketing opt-in. Read those as directional operating ranges rather than guarantees; they vary with placement, incentive, and checkout flow. The comparison that matters is with the status quo, where in-store identification for non-members rounds to zero.

For a fuller treatment of how receipt capture complements an existing app strategy, see our post on how digital receipts capture the customers your retail app misses.

Frequently asked questions

What is a single customer view in retail?

A single customer view is one unified customer profile that combines identity, transactions, and engagement from every channel, online and in-store, into a single record. It is the foundation for personalisation, attribution, and lifetime value measurement, and it requires identifying customers in physical stores, where most retail transactions still happen.

How do you integrate online and offline customer data?

Both sides need a shared identifier. Online data already carries one through logins and checkout emails. In-store, an identification moment must be added at the point of sale, most practically through digital receipts, so the transaction links to a profile that flows by API into the same CDP or CRM as the online data.

How do you create a single customer view without replacing your CRM or CDP?

Add an identification layer at checkout rather than a new platform. Receipt-led identification creates profiles at the point of sale and delivers them into the existing stack through APIs, so Salesforce Marketing Cloud, Selligent, mParticle, or a comparable system remains the system of record and simply starts receiving in-store data.

Why are most in-store customers anonymous?

Physical stores have no built-in identification moment. Online, identity arrives automatically through accounts, emails, and cookies. In-store, a customer can select products, pay by card or cash, and leave without any step that captures who they are. Loyalty programmes identify members only, and members are a minority of transactions.

How do digital receipts identify in-store customers?

A QR code at checkout replaces or accompanies the printed receipt. Scanning it opens the receipt in the browser and creates an anonymous profile linked to the full basket. When the customer adds an email address and opts in, the profile becomes a known, reachable contact, with no app download or loyalty enrolment required.

Is receipt-based customer identification GDPR compliant?

It can be run fully GDPR compliant, and the structure helps. Consent is collected explicitly from the customer at the moment of capture, tied to a real interaction, and logged per profile. That is a more defensible basis than cashier-collected details or inferred identifiers, though the retailer’s own privacy setup and disclosures still apply.

The store was never the problem

Variety and lifestyle retail did not fall behind on customer data. It built CDPs, loyalty programmes, and campaign engines that the rest of physical retail still lacks. The half-finished part is the input: the store, the channel carrying most of the volume, was never instrumented to say who was in it. The receipt already sits at the end of every one of those transactions. Identification can too.

If you want to see what in-store identified profiles look like flowing into your own CRM, talk to us and we will show you with your stack, not a slide.